Mortgage Investment Corporation for Dummies

Mortgage Investment Corporation for Dummies

Blog Article

The Main Principles Of Mortgage Investment Corporation

Table of Contents6 Easy Facts About Mortgage Investment Corporation ExplainedThe Ultimate Guide To Mortgage Investment CorporationSome Known Facts About Mortgage Investment Corporation.Not known Details About Mortgage Investment Corporation 3 Easy Facts About Mortgage Investment Corporation Shown

Does the MICs credit history board testimonial each mortgage? In most scenarios, mortgage brokers manage MICs. The broker needs to not work as a participant of the credit report board, as this puts him/her in a direct conflict of passion offered that brokers generally gain a compensation for placing the mortgages. 3. Do the directors, members of credit committee and fund supervisor have their very own funds invested? An of course to this question does not provide a safe investment, it must provide some boosted safety if evaluated in combination with various other sensible loaning plans.Is the MIC levered? The financial organization will approve certain mortgages owned by the MIC as safety and security for a line of credit score.

It is essential that an accountant conversant with MICs prepare these declarations. Thank you Mr. Shewan & Mr.

6 Simple Techniques For Mortgage Investment Corporation

This does not indicate there are not threats, yet, normally speaking, regardless of what the wider stock market is doing, the Canadian realty market, particularly significant city locations like Toronto, Vancouver, and Montreal does well. A MIC is a firm formed under the regulations set out in the Revenue Tax Obligation Act, Section 130.1.

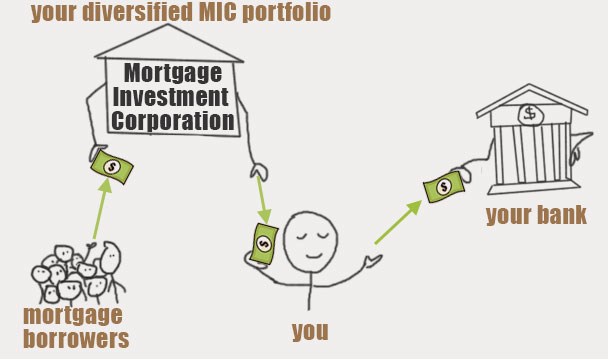

The MIC earns revenue from those home loans on rate of interest fees and general costs. The genuine charm of a Home loan Investment Firm is the yield it offers financiers contrasted to various other fixed income financial investments. You will have no trouble locating a GIC that pays 2% for a 1 year term, as federal government bonds are equally as reduced.

Facts About Mortgage Investment Corporation Revealed

There are stringent needs under the Income Tax Obligation Act that a company must fulfill prior to it qualifies as a MIC. A MIC has to be a Canadian corporation and it should spend its funds in mortgages. MICs are not allowed to handle or create real estate building. That claimed, there are times when the MIC winds up possessing the mortgaged property due to foreclosure, sale contract, and so on.

A MIC will certainly earn interest income from mortgages and any cash the MIC has check my reference in the bank. As long as 100% of the profits/dividends are provided to shareholders, the MIC does not pay any type of revenue tax obligation. Rather of the MIC paying tax on the passion it earns, investors are liable for any kind of tax.

MICs issue common and recommended shares, providing redeemable favored shares to investors with a repaired returns price. These shares are taken into consideration to be "certified financial investments" for deferred earnings plans. This is suitable for capitalists who purchase Home mortgage Financial investment Firm shares with a self-directed registered retired life savings strategy (RRSP), registered retired life earnings fund (RRIF), tax-free savings account (TFSA), postponed profit-sharing strategy (DPSP), registered education and learning financial savings plan (RESP), or signed up special needs cost savings plan (RDSP).

And Deferred Strategies do not pay any tax obligation on the passion they are approximated to obtain. That stated, those that hold TFSAs and annuitants of RRSPs or RRIFs might be hit with particular charge tax obligations if the financial investment in the MIC is considered to be a "forbidden investment" according to Canada's tax code.

What Does Mortgage Investment Corporation Mean?

They will certainly ensure you have discovered a Home mortgage Financial investment Firm with "competent investment" standing. If the MIC qualifies, maybe really helpful come tax time given that the Related Site MIC does not pay tax obligation on the interest income and neither does the Deferred Plan. Mortgage Investment Corporation. A lot more generally, if the MIC falls short to fulfill the demands established out by the Revenue Tax Obligation Act, the MICs revenue will be strained prior to it obtains dispersed to investors, decreasing returns considerably

It shows up both the real estate and supply markets in Canada go to perpetuity highs On the other hand yields on bonds and GICs are still near document lows. Also cash is losing its allure since power and food rates have actually pushed the rising cost of living price to a multi-year high. Which asks the question: Where can we still discover value? Well I think I have the response! In May I blogged regarding considering home loan financial investment firms.

The 20-Second Trick For Mortgage Investment Corporation

If rate of interest rise, a MIC's return would likewise increase because higher home mortgage prices suggest even more revenue! People that buy a home loan investment corporation do not have the realty. MIC capitalists just make money from the enviable position of being a lender! It resembles peer to peer try this loaning in the united state, Estonia, or other parts of Europe, other than every funding in a MIC is safeguarded by real estate.

Many difficult functioning Canadians who want to acquire a house can not obtain home mortgages from typical banks due to the fact that possibly they're self utilized, or do not have a well established credit rating background. Or perhaps they want a brief term funding to create a huge residential or commercial property or make some restorations. Banks have a tendency to overlook these prospective consumers because self utilized Canadians don't have stable incomes.

Report this page